Best Billing Software For Stationery Shops

Simplify billing, track inventory, and manage accounts effortlessly.

Trusted by 1 Crore+ Businesses Across India

What is Billing Software for Stationery Shop?

Billing software for stationery shop is a specialized tool designed to streamline the billing and invoicing processes for businesses selling stationery items. Similar to billing software for retail shops, it helps stationery shop owners manage their sales, generate GST-compliant invoices, track inventory, and handle payments efficiently. This software enables smooth management of daily transactions, simplifies stock management, and provides real-time data on sales and customer details. With features like customizable invoices, expense tracking, and stock management, billing software for stationery shops helps improve operational efficiency and ensure accurate financial records.

Key Features of Billing Software for Stationery Shops

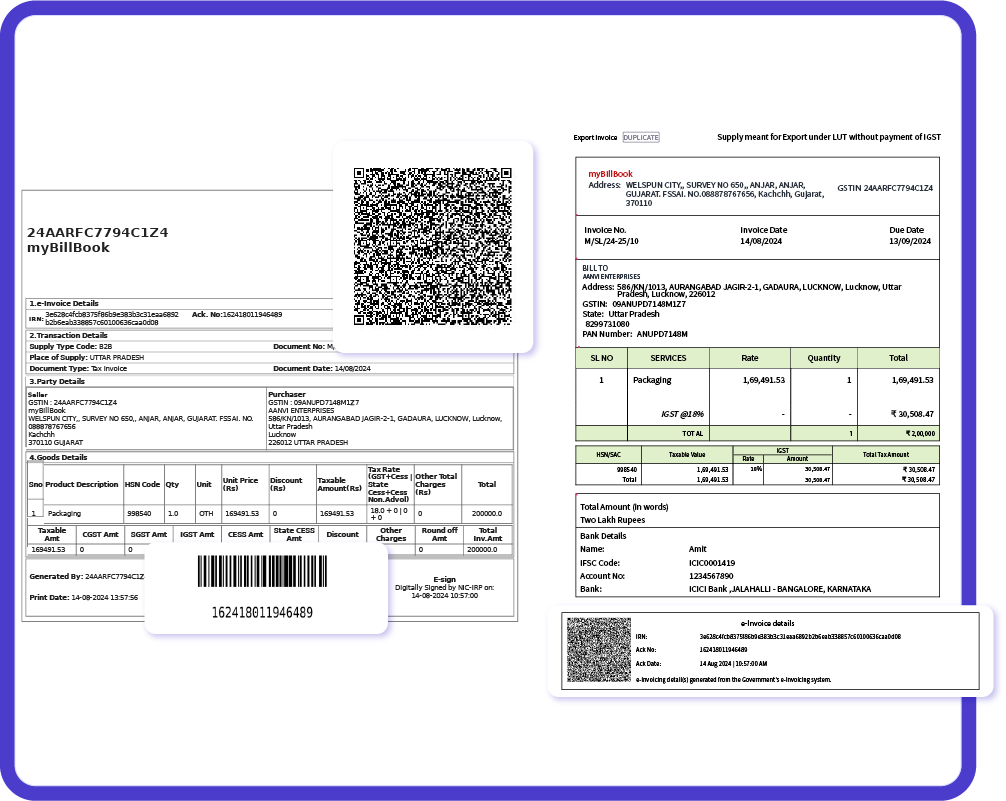

Quick & Easy Invoicing

Generate GST and non-GST bills within seconds, whether selling single items or bulk stationery supplies. Save frequently sold items for faster billing and reduce manual entry efforts.

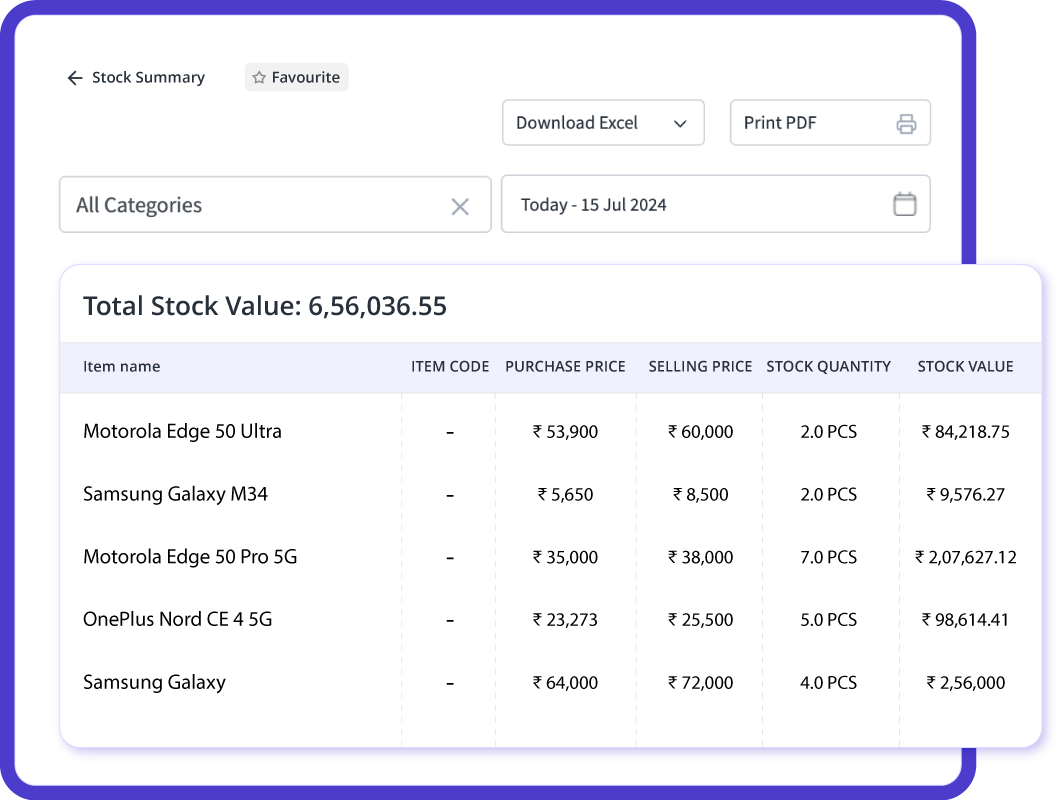

Inventory & Stock Management

Keep track of fast-moving and slow-moving items, get stock alerts, and manage multiple product categories efficiently. Avoid overstocking or running out of essential items with real-time inventory updates.

Barcode Scanning for Faster Billing

Scan barcodes of books, notebooks, pens, and other stationery items to automatically fetch product details and prices, speeding up checkout. Minimize billing errors and enhance the customer experience with quick scanning.

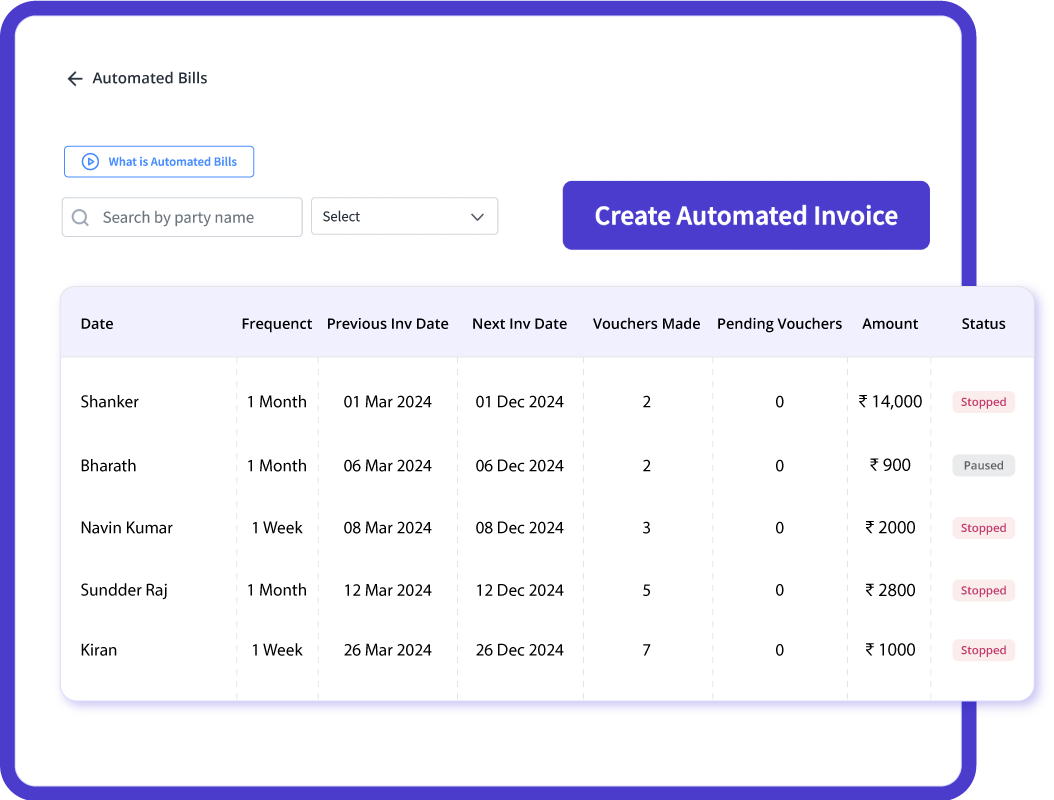

Customer Credit & Payment Tracking

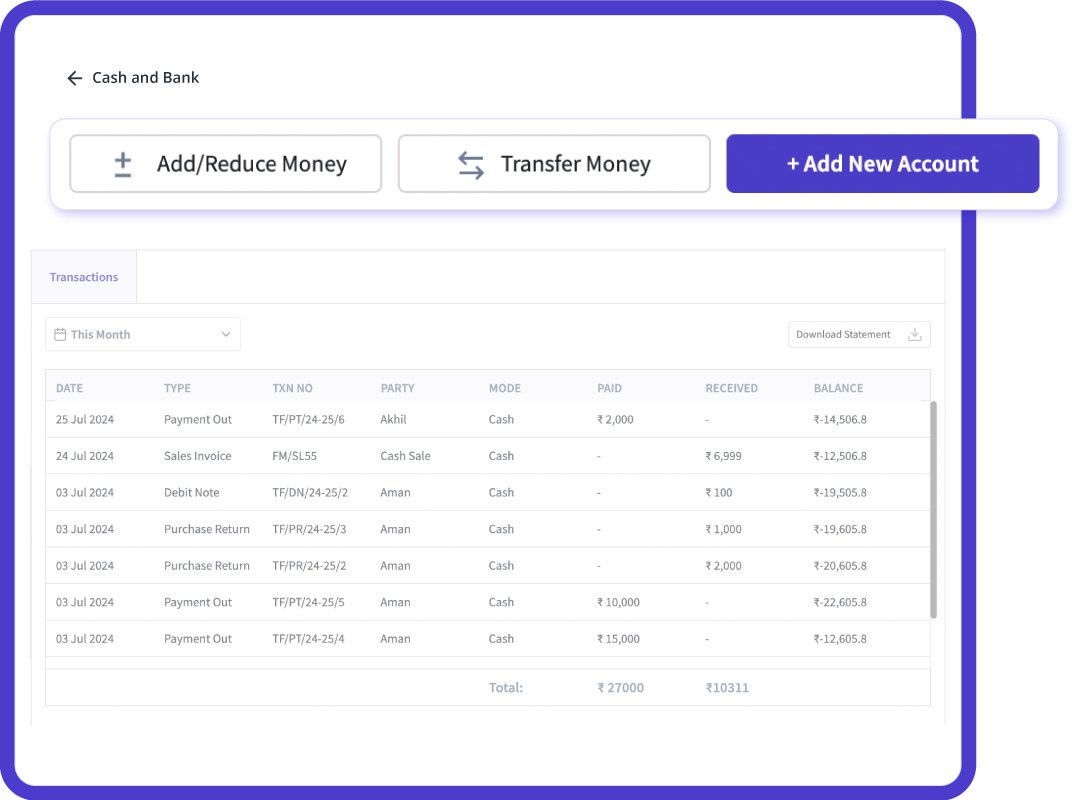

Record credit sales, track outstanding payments, and send automated reminders for pending dues. Maintain clear records of customer transactions and improve cash flow management.

Multi-Payment Mode Support

Accept payments via cash, UPI, credit cards, and wallets, ensuring smooth transactions for customers. Offer flexible payment options to enhance customer satisfaction and convenience.

Print & Digital Bill Sharing

Instantly print invoices or share them via WhatsApp, email, or SMS, making it convenient for customers and reducing paper usage. Improve business branding with customizable invoices that include your shop name and logo.

Product Demo of Billing Software for Gift & Stationery Shops

myBillBook helps Business succeed

“Stocking seasonal gifts and fast-moving stationery used to be challenging. MyBillBook’s low-stock alerts and detailed sales reports help me plan better and avoid overstocking or shortages.”

Sneha Kapoor,

Stationery Store Owner

“Earlier, I struggled with manual billing and keeping track of customer payments. MyBillBook’s automated invoicing and payment reminders ensure I get paid on time while keeping my accounts organized.”

Amit Sinha,

Gift & Stationery Retailer

“With MyBillBook, I can now generate GST-compliant invoices, track expenses, and manage supplier payments seamlessly. It has simplified my business operations and saved me valuable time.”

Poonam Verma,

Gift & Stationery Wholesaler

Pricing plans

Diamond Plan

₹217

Per month. Billed annually. Excl. GST @18%

✅ Create unlimited invoices

✅ Add up to 1 business + 1 user

✅ Inventory management

✅ App + Web support

✅ Priority customer support

✅ GSTR reports in JSON format Popular

Platinum Plan

₹250

Per month. Billed annually. Excl. GST @18%

Everything on Diamond Plan +

✅ Add up to 2 business + 2 user

✅ 50 e-Way bills/year

✅ Staff attendance + payroll

✅ Godown management

✅ Whatsapp and SMS marketing Popular

Enterprise Plan

₹417

Per month. Billed annually. Excl. GST @18%

Everything on Platinum Plan +

✅ Custom invoice themes

✅ Create your online store

✅ Generate and print barcode

✅ POS billing on desktop app

✅ Unlimited e-Invoices & e-Way bills

Billing Software for Stationery Shops – Simplify Invoicing & Inventory Management

Smart Billing Solution for Stationery Stores

Running a stationery shop involves managing a wide range of products, from notebooks and pens to office supplies and art materials. With frequent stock movement, customer purchases, and bulk orders, handling billing and inventory manually can become overwhelming. A digital billing system not only speeds up the invoicing process but also helps keep track of stock levels, customer credit, and payments effortlessly.

With myBillBook Billing Software for Stationery Shops, you can generate invoices in seconds, manage stock efficiently, and track payments digitally—all from one platform. Whether you run a small stationery shop, an office supply store, or a wholesale stationery business, this software ensures error-free billing and smooth inventory management.

Why Do Stationery Shops Need Billing Software?

A stationery business deals with a high volume of small-value transactions daily. Manually entering product details, calculating GST, and managing inventory can be time-consuming and prone to errors. A stationery billing software automates these processes, making billing faster, more accurate, and hassle-free.

Here’s how it can help:

- Generate professional invoices instantly – Create GST & non-GST invoices with accurate tax calculations.

- Simplify inventory tracking – Monitor stock levels and get low-stock alerts to avoid running out of popular items.

- Manage customer credit & outstanding payments – Keep track of pending payments and send automated reminders.

- Apply discounts & offers easily – Run promotions and apply bulk order discounts directly in invoices.

- Accept multiple payment methods – Record payments via cash, UPI, credit/debit cards, or wallets effortlessly.

- Digitally share invoices with customers – Send invoices via WhatsApp, email, or SMS, reducing paper usage.

Who Can Use This Billing Software?

- Retail Stationery Shops – Easily create invoices, manage stock, and track daily sales.

- Office & School Supply Stores – Handle bulk orders, apply discounts, and maintain supplier records.

- Wholesale Stationery Distributors – Generate large invoices, manage inventory, and streamline credit transactions.

- Book & Stationery Suppliers – Track product batches, apply GST, and organize stock efficiently.

Common Challenges in Stationery Billing & How Software Solves Them

Many stationery shop owners face common challenges in their day-to-day operations. Here’s how myBillBook Billing Software helps resolve them:

- Slow billing process – Manual invoice creation can slow down checkout, causing long queues. The software enables fast barcode scanning for quick billing.

- Inventory mismanagement – Running out of essential stationery items can affect sales. Real-time stock updates help avoid shortages and overstocking.

- Manual tax calculations – GST errors in invoices can lead to compliance issues. The software auto-applies GST rates for accurate invoicing.

- Tracking customer credit manually – Managing pending dues can be difficult. The software records credit transactions and sends automated payment reminders.

- Paper invoices getting lost – Customers may misplace physical bills. The software allows you to print or digitally share invoices instantly.

Benefits of Using Billing Software for Stationery Shops

- Saves Time & Reduces Errors – Automates billing, tax calculations, and inventory updates, reducing manual mistakes.

- Increases Billing Speed – Barcode scanning and quick product selection make checkout faster.

- Manages Stock Efficiently – Low-stock alerts ensure timely restocking of fast-moving items.

- Improves Financial Management – Tracks cash flow, outstanding payments, and profits accurately.

- Enhances Customer Satisfaction – Digital invoices, easy returns, and multiple payment options create a seamless shopping experience.

Why myBillBook is the Best Billing Software for Stationery Businesses

Choosing the right billing software for your stationery shop is crucial for streamlining daily operations, managing inventory, and ensuring seamless transactions. myBillBook stands out as the best billing solution for stationery businesses due to its user-friendly interface, automated features, and flexibility to cater to both small retailers and large wholesalers. Here’s why myBillBook is the perfect choice for your stationery business:

1. Easy-to-use interface for Quick Billing

myBillBook is designed with a simple and intuitive interface, allowing even first-time users to generate invoices effortlessly. You don’t need advanced technical skills—just a few clicks, and you can create professional invoices with itemized details, GST calculations, and payment breakdowns.

2. Faster Checkout with Barcode Scanning

Stationery shops deal with a large variety of products, making manual billing time-consuming. myBillBook supports barcode scanning, allowing you to add products to the invoice instantly. This speeds up the billing process, minimizes errors, and enhances customer experience by reducing wait times.

3. Automated GST & Discount Calculations

Tax compliance can be challenging for businesses dealing with different types of stationery items. myBillBook automatically applies GST rates based on product categories, ensuring error-free taxation. Additionally, you can set up bulk discounts, promotional offers, or seasonal sales, which are applied automatically during invoicing.

4. Real-Time Inventory Management

Keeping track of stationery stock manually can lead to overstocking or running out of essential items. myBillBook offers real-time inventory tracking, notifying you when stocks are low or when popular items need restocking. This helps you manage your supply chain efficiently and avoid missed sales due to stock unavailability.

5. Customer Credit & Outstanding Payment Tracking

Many stationery shop owners sell products on credit, especially to schools, offices, and bulk buyers. myBillBook keeps a record of customer credit transactions and helps you track outstanding payments. You can also send automated reminders via WhatsApp, SMS, or email, ensuring timely payments without manual follow-ups.

6. Multi-Payment Mode Support

With customers preferring different payment methods, myBillBook allows you to accept payments via cash, UPI, credit/debit cards, and digital wallets. This flexibility ensures smooth transactions and enhances customer convenience.

7. Print or Share Invoices Instantly

Stationery shops often need to provide printed invoices for customers or suppliers. With myBillBook, you can instantly print invoices or share them digitally via WhatsApp, email, or SMS, reducing paper usage and making transactions more efficient.

8. Cloud-Based Access for Anytime, Anywhere Management

Unlike traditional billing software that stores data on a local computer, myBillBook is cloud-based, allowing you to access invoices, stock details, and reports from anywhere. Whether you are at your shop, home, or traveling, you can manage your business remotely from your mobile or desktop.

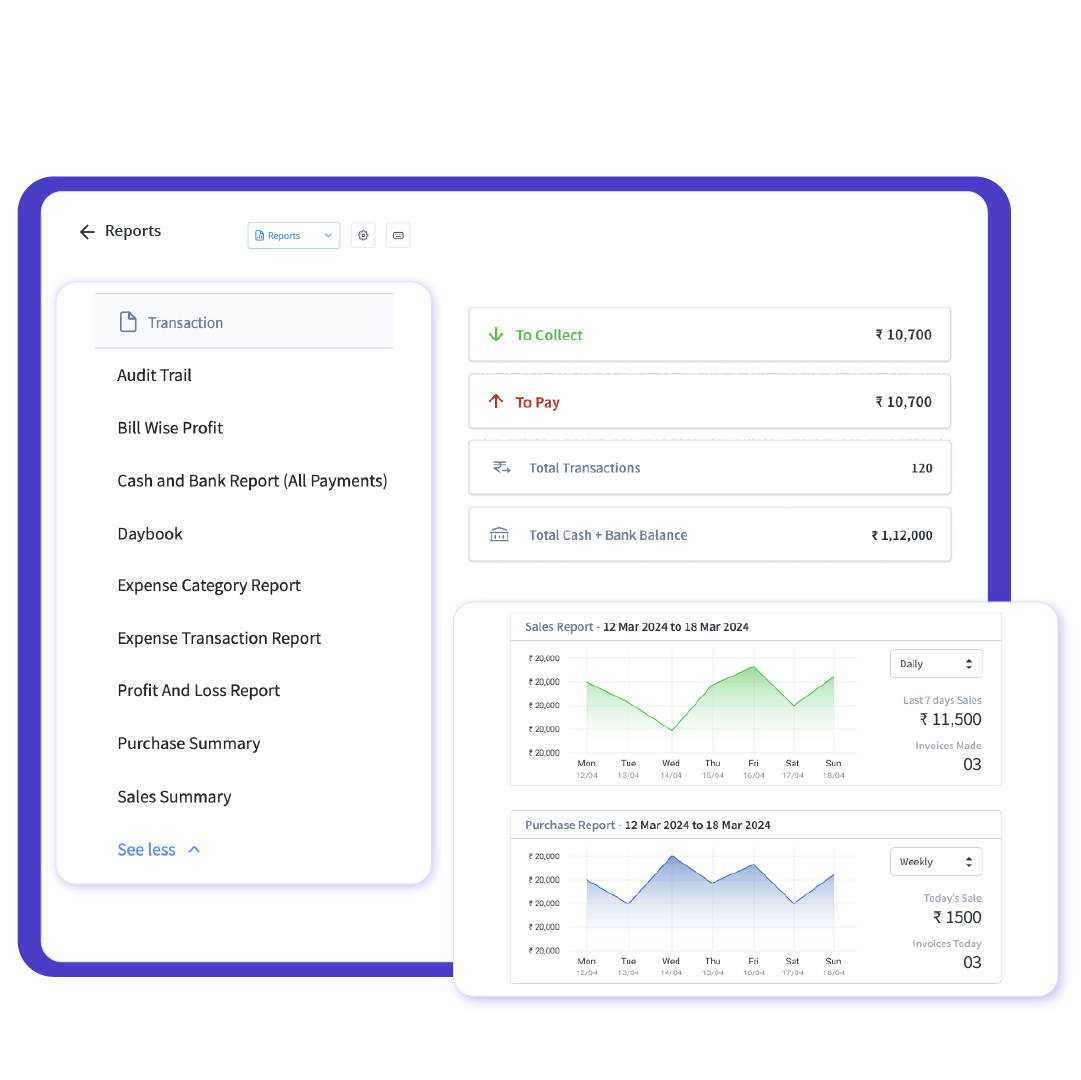

9. Business Reports & Sales Insights

Understanding your business performance is essential for growth. myBillBook generates detailed business reports, including sales trends, profit & loss statements, stock movement, and outstanding payments. These insights help you make informed business decisions and improve profitability.

10. Secure Data Backup & Easy Migration

Losing invoice records or stock data can be a major setback for any business. myBillBook offers automatic data backup, ensuring your records are safe. If you are shifting from manual billing or another software, easy data migration features help you transfer all your records without hassle.

FAQs

1. How can myBillBook help in managing my stationery shop’s billing?

myBillBook simplifies invoice creation with GST & non-GST formats, supports barcode scanning for faster billing, and allows digital sharing of invoices via WhatsApp, email, or SMS. It also provides automated tax calculations and multiple payment options to streamline transactions.

2. Can I track my stationery stock using myBillBook?

Yes, myBillBook offers real-time inventory tracking, helping you monitor stock levels, avoid overstocking, and get alerts for low-stock or fast-moving items. It ensures that you always have the right products available for customers.

3. Does the software allow credit sales and outstanding payment tracking?

Yes, you can record credit sales, track outstanding payments, and send automated reminders to customers via WhatsApp or SMS. This helps in managing dues efficiently and improves cash flow.

4. Can I accept different payment methods with myBillBook?

myBillBook supports multiple payment modes, including cash, UPI, credit/debit cards, and digital wallets, making transactions smoother for your customers.

5. Is my data safe with myBillBook?

Yes, myBillBook is cloud-based, meaning all your invoices, stock details, and customer records are securely stored and automatically backed up. You can access your business data anytime, from anywhere.