Petty Cash Book Format

Track small business expenses with ease using our free downloadable Petty Cash Book formats. Whether you’re maintaining a simple columnar record or need detailed expense categorization, myBillBook billing software provides professional, GST-friendly petty cash templates that make accounting hassle-free.

Download free, editable petty cash book templates – Simple, Quick & GST-Ready.

For complete expense documentation, businesses also use standard Invoice Format templates to record purchases, reimbursements, and payable expenses accurately.

Download Free Petty Cash Book Formats

Unlock Premium and Luxury Invoice Templates

Features of myBillBook Petty Cash Book Format

Easy Cash Flow Monitoring

Record every petty cash expense in real time and automatically track your remaining balance to avoid overspending or manual miscalculations.

Pre-Defined Expense Categories

Categorise petty expenses like courier, tea, stationery, and travel. It saves time, improves reporting, and reduces confusion during reconciliation.

User Access Control

Restrict access to petty cash records by assigning user roles. Prevent misuse, ensure accountability, and maintain an accurate audit trail for all entries.

Automated Reconciliation

Easily match petty cash entries with uploaded bills or vouchers. MyBillBook helps you identify mismatches quickly and keep your books clean.

Mobile & Desktop Friendly

Manage your petty cash book from anywhere using the MyBillBook mobile app or desktop software. Ideal for shop owners, managers, or accountants on the move.

Downloadable Reports & Audit Trails

Generate monthly or weekly petty cash reports with a single click. Perfect for audits, compliance, or internal reviews.

What is a Petty Cash Book?

A petty cash book is a record used by businesses to track minor cash expenses such as stationery, travel, snacks, or courier charges. Instead of processing each small payment via bank, companies allocate a fixed petty cash fund to a cashier who records every usage in the petty cash book.

There are typically two formats:

- Columnar Format: Simple layout with date, voucher no., particulars, amount, and balance.

- Analytical Format: Includes categorized columns like Postage, Stationery, Travel, etc.

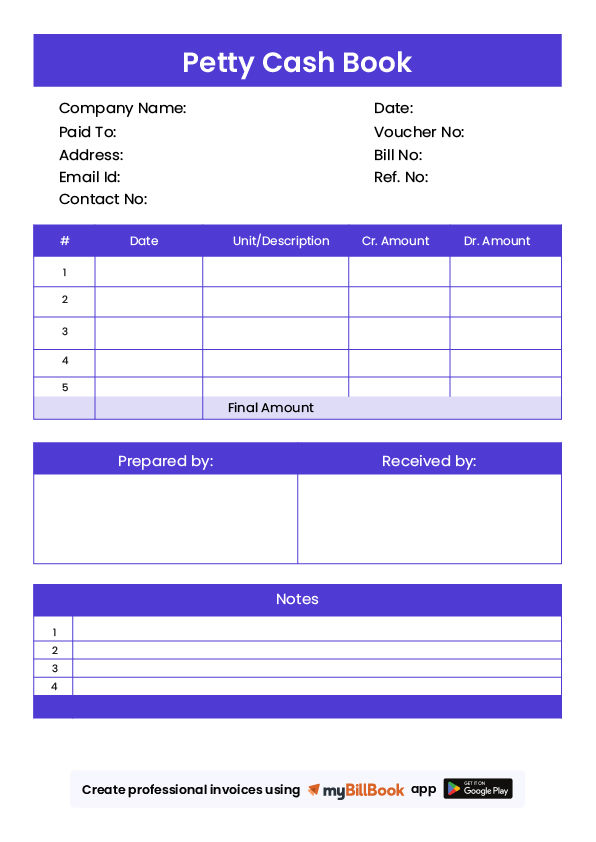

Format of Petty Cash Book

A petty cash book is usually a small notebook or ledger to record all small cash transactions. The format of the petty cash book may vary depending on the organisation’s specific needs and requirements.

- Heading: The petty cash book should have a clear and concise heading

- Date: The date column records the date on which the transaction occurred. This column should be left-aligned.

- Description: The description column records the purpose of the transaction, such as postage, office supplies, or other small expenses. This column should be left-aligned.

- Voucher Number: If the petty cash system uses vouchers, this column records the voucher number for the transaction. This column should be centre aligned.

- Amount: The amount column records the amount of the transaction. This column should be right-aligned.

- Debit/Credit: This column indicates whether the transaction is a debit or a credit. This column should be centre aligned.

- Balance: The balance column records the remaining balance of the petty cash fund after each transaction. This column should be right-aligned.

How to Use the Petty Cash Book Templates

- Download the Excel format (Columnar or Analytical).

- Set opening balance based on your business float.

- Enter transactions regularly with voucher no. and purpose.

- Monitor balance and reconcile periodically.

- Attach vouchers for better audit trail.

🔄 Columnar vs Analytical: Which Format Should You Use?

| Feature | Columnar Format | Analytical Format |

| Simplicity | ✅ Simple to use | ❌ Slightly complex |

| Categorization | ❌ No categories | ✅ Tracks by expense type |

| Ideal For | Small shops, retail | Offices with multiple expense heads |

| Example Use Case | Stationery, snacks, etc. | Travel, Postage, Printing, Staff Welfare |

How to Maintain a Petty Cash Book

The petty cash book can be maintained manually or using the software. However, manual bookkeeping is more common in small businesses. To create a manual cash book, you need to follow these simple steps:

Step 1: Create a Petty Cash Fund

Before creating a petty cash book, you need to establish a petty cash fund. The amount of petty cash funds depends on the size of the business and the number of petty cash expenses incurred. Usually, the amount is kept between Rs.5,000 and Rs.10,000. The fund is typically kept in a safe or locked drawer in the office.

Step 2: Choose a Petty Cash Book

Select a petty cash book that meets your business requirements. It should have columns to record the date, description, amount, and the person or department responsible for the expense. Some books have additional columns to record the receipts and the balance of the cash fund.

Step 3: Record the Opening Balance

Record the opening balance of the petty cash fund. This is the amount of cash that is available in the fund.

Step 4: Record Expenses

Whenever a small cash expense is made, the transaction should be recorded in the petty cash book. The person who made the expense should fill out a petty cash voucher, including the date, description, and amount of the expense. The voucher should also include the person or department responsible for the expense. The voucher should be attached to the receipt and kept in the petty cash book for future reference.

Step 5: Reconcile the Petty Cash Book

Periodically, you should reconcile the petty cash book to ensure that the amount of cash in the fund matches the transactions recorded in the book. To do this, add up all the expenses recorded in the petty cash book and subtract them from the opening balance. The result should be the cash left in the petty cash fund. If there is a difference, you need to investigate and find out the reason for the discrepancy.

Petty Cash Maintenance

Two main systems are followed for petty cash maintenance: the Imprest system and the Non-imprest system.

Imprest System: The most common and widely used method of maintaining petty cash. A fixed amount of money is set aside for petty cash, and a cashier is appointed to manage it. The cashier is responsible for maintaining, recording, and reconciling the petty cash fund at the end of each period. He will request reimbursement from the finance department to restore the fund to its original amount when it is depleted.

Non-Imprest System: No fixed amount of money is set aside in this system. Instead, the finance department replenishes the petty fund as and when required by the finance department, based on receipts or vouchers submitted by the cashier. This system is typically used when petty cash transactions are irregular and cannot be predicted in advance.

While the imprest system provides greater control over petty cash and helps to prevent the misappropriation of funds, the non-imprest system provides greater flexibility in managing petty cash. Further, the latter requires more administrative effort to maintain accurate records of all transactions. Ultimately, the type of petty cash maintenance a company chooses depends on its specific needs, the volume of petty cash transactions, and the level of control required over the fund disbursements.

Use myBillBook billing and invoicing software to manage all your bookkeeping tasks accurately and efficiently.

Frequently Asked Questions

What is the ideal frequency to update the petty cash book?

You should update it daily or every time a new expense is made.

Can I use Excel or PDF formats to maintain a petty cash book?

Yes, both Excel and PDF formats are commonly used to record petty cash transactions. myBillBook offers free downloadable petty cash book templates in both formats.

Can I attach vouchers or bills to entries in myBillBook?

Yes, myBillBook lets you upload receipts or vouchers as attachments.

How is petty cash different from regular business expenses?

Petty cash is meant for small, everyday expenses like tea, stationery, or courier charges. Regular expenses are typically larger and recorded through standard accounting processes.

Is it mandatory to maintain a petty cash book for small businesses?

It’s not mandatory under law, but it’s a best practice for internal control.

Who is responsible for managing petty cash in a business?

Usually, a cashier or petty cash custodian is assigned to manage petty cash. They are responsible for recording expenses and maintaining receipts.

What happens when the petty cash runs out?

A top-up is done to replenish it back to the imprest amount after reconciliation.

Can I track multiple petty cash accounts in myBillBook?

Yes, myBillBook allows businesses to manage multiple petty cash accounts across locations or departments, making tracking more organised and transparent.

Know More About Bill Formats