On the 7th of June, 2021, the Income Tax Department has announced an update about its new e-filing website that has been soon going to replace the current

portal www.incometaxindiaefiling.gov.in.

This new portal would be user-friendly thereby offering a great e-filing experience to the taxpayers. In fact, this website makes sure that the taxpayers should have a seamless and quick ITR filing process. At present, filing of ITR1, ITR2, and ITR 4 is possible on the new portal and the taxpayers can have the new ITR filing software free of cost. As this article is all about the facts of filing the ITR4 form, we should look at it in a detailed way. The taxpayers who issue their income tax return under section 44 AD of the Income Tax Act, 1961 should submit the ITR 4 form to get the advantages of the presumptive taxation scheme. This scheme eases the undertaking of small-scale businesses by avoiding the monotonous task of maintaining their accounts and books.

What is ITR 4?

ITR-4 form is an income tax return form filed by those taxpayers who have selected the presumptive income scheme under Section 44AD, Section 44AE, and Section 44ADA and whose earnings do not exceed Rs. 50 lakhs. On the other hand, if the business turnover given above is more than Rs. 2 crores, the taxpayer would need to file ITR-3.

Who can File ITR 4?

As mentioned above, ITR 4 means income tax return that is submitted by those registered taxpayers who have opted for the presumptive income scheme as per section 44 AD of the Income Tax Act, 1961. The ITR4 is issued by the Partnership firm or HUF or individuals whose sum of income of AY 2020-21 comprises as given below:

- Earnings from a profession that comes under section 44ADA

- Business income as per section 44AE or 44AD

- Earnings from other sources that are of up to Rs. 50 lakhs (except earnings from horse races and winning from the lottery)

- Earnings from One House Property that is of up to Rs. 50 lakhs (except the loss to be carried forward or brought forward loss cases under this head)

- Income in the form of salary or pension that is of up to Rs. 50 lakhs.

It is to be noted that freelancers involved in the profession mentioned above can also choose this scheme if their gross receipts do not go more than Rs. 50 lakhs.

Who is not Required to File ITR4 for 2021-2022?

Let us have a look at those individuals who do not need to submit ITR4 for the assessment year 2021-2022 which are as follows:

- A person, partnership enterprise, or HUF whose books of accounts should be calculated as per the Income Tax Act, 1961.

- A person who has invested in unlisted equity shares or is a director in a company cannot make use of this form.

- A person who has earnings or income from house property, salary, or other sources with the limit of above Rs. 50 lakhs cannot use this form.

What is the Change in ITR4 in 2021-22?

There are several changes that have been made in ITR4 of the assessment year 2021-2022 which are given below:

- ITR4 form cannot be issued when it comes to deferment of tax on ESOPs

- This form should be made into use by a registered taxpayer to file the income tax return for 2021-2022.

- In the case of the ITR4 form, the exercise of option has been authorized as per section 115BAC.

How to File ITR 4?

You can either file ITR4 online through an e-filing portal or offline through an offline utility. To file the form through online mode, you can check out the steps given below:

Step 1: Visit the e-filing portal and log in using your valid credentials.

Step 2: Once you land on the dashboard, click the options e-File 🡪 Income Tax Returns 🡪 File Income Tax Return as shown below. Then in the page that opens you can follow these steps.

- Choose financial year as 2021-22 and hit the option CONTINUE

- Choose the mode of filing as online and then press PROCEED

- As applicable, select status and click the option CONTINUE to go with the further process.

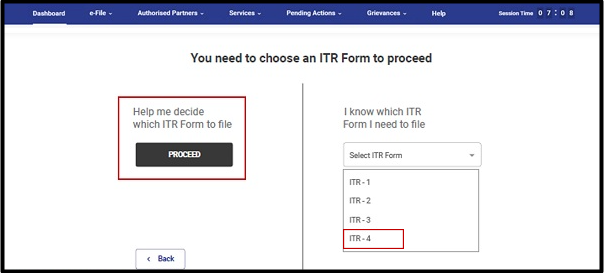

Step 3: Choose ‘Help me decide which ITR Form to file’ and hit ‘Proceed’. Once you get the right ITR from the system, you can go ahead with filing your ITR. Go through the instructions carefully to fill the form and keep the list of required documents in mind and press ‘Let’s Get Started.’ Choose the checkboxes that apply to you and hit ‘Continue’.

Step 4: Check out all of your pre-filled details and edit if required. If necessary, enter the additional details and click ‘Confirm’ right at the end of each portion.

- Fill in the details of your income and deduction in another section. Once you complete and confirm all the portions of the form, you can click ‘Proceed’. However, there are two options to follow as per the condition.

- In case if there is a need to pay tax liability based on the computation, you will get the options ‘Pay Now’ and ‘Pay Later’ at the end of the page.

- If the condition is reverse which means after paying tax, if there is a refund or no tax liability payable based on tax computation, you will be redirected to the page ‘Preview and Submit Your Return’.

Step 5: Once you reach the ‘Preview and Submit Your Return’ page, you have to fill location, choose the declaration checkbox, and hit ‘Proceed to Validation’.

Step 6: Once validation has been done on your Preview and Submit your Return page, you can click ‘Proceed to Verification.’

Step 7: Choose your applicable option on the Complete your Verification page and press ‘Continue’.

Step 8: Once you get into the page of e-Verify, choose your preferred option through which you need to e-Verify the return and hit ‘Continue’.

FAQs on ITR 4

Q. Where to show speculation loss in ITR 4?

Ans: Speculative business is treated as a separate business for setting off the loss provisions. Under Section 73, speculation business losses can be resolved only against speculative business profits. However, other business losses can be set off against any business profits. Moreover, speculation business loss carried forward to the following year can be set off only against the gains or profits of any speculative business in the succeeding year.

Speculation business transactions are considered as intra-day trading according to Section 43(5) of the Income Tax Act, 1961 and the earnings generated would be either speculation profits or speculation losses. However, earnings from speculation profits are taxed at reasonable rates. Speculation loss can be claimed in ITR 4 if Tax Audit u/s 44AD is undertaken by a professional Chartered Accountant. The speculation loss can be carried forward and set forth against future speculation gains to decrease the income tax liability.