Sales Report: Meaning, Types, Format and Examples

Learn what a sales report is, its types, format, key metrics, and practical examples for Indian small businesses.

Read Articles on GST

Learn what a sales report is, its types, format, key metrics, and practical examples for Indian small businesses.

Improve billing accuracy, reduce payment delays, and organise GST invoices with 25 practical invoicing tips for Indian small businesses.

See how AI is changing India’s tax system for businesses through GST data, e-invoicing, fraud checks, and smarter compliance.

In India, billing is closely tied to GST compliance, invoice records, and payment tracking—so choosing the right billing type isn’t

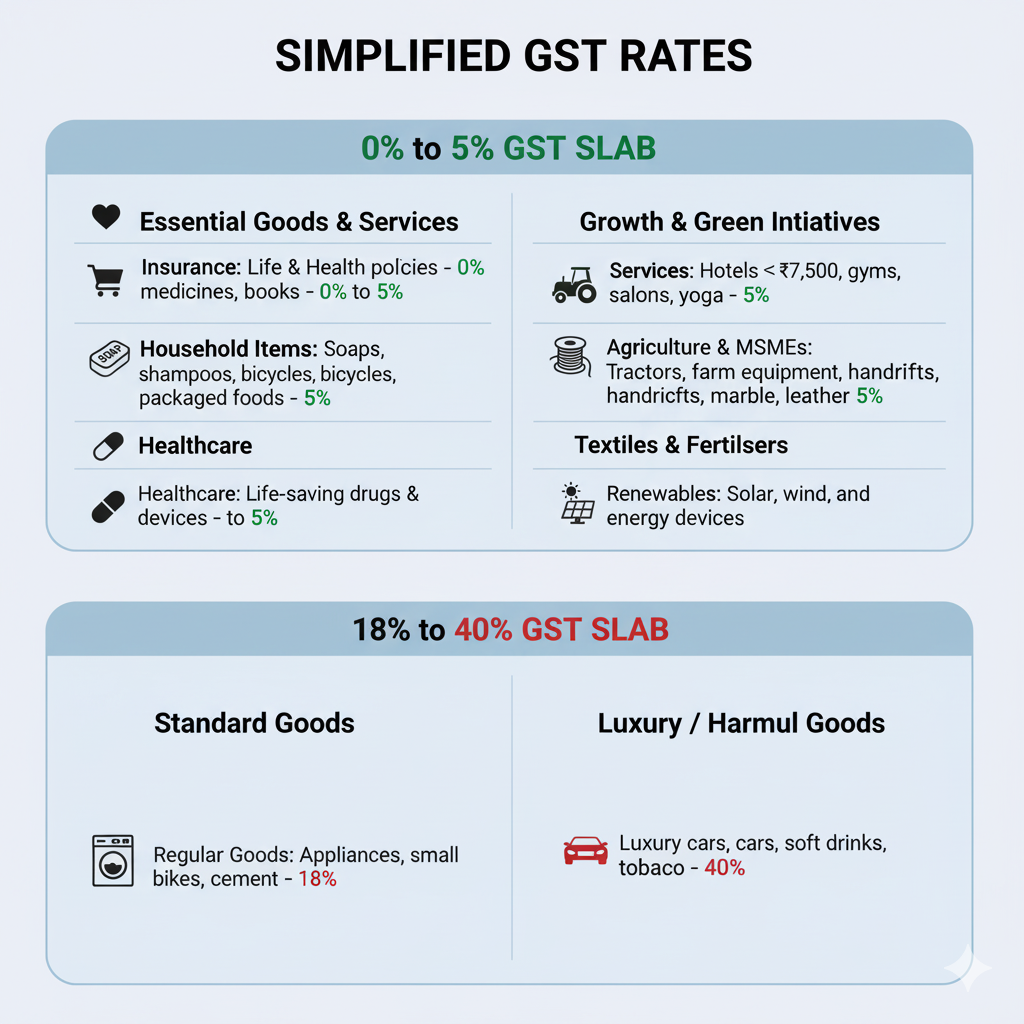

The Next-gen GST Reforms 2025 have been approved and announced by the Finance Minister of India in the 56th meeting

Small and medium enterprises (SMEs) contribute to more than 45% of manufacturing output in India. Besides, more than 40% of

An e Way Bill is a document essential for transporting goods worth more than ₹50,000 in India under the Goods

The coming of e-way bills has standardised compliance documents while transporting goods across states. However, issuing e-way bills during transport is not

Gujarat, the jewel of the west, has been a significant state involved in business for a while now. Hence the