Income Tax Return has several forms, and people are required to file each form based on their business or profession and income from these. Anybody who falls under the benchmark of ITR must mandatorily file the ITR without any fail. This guide is all about ITR 3, and you can learn about who can file ITR 3 and what are the changes made to this ITR form, and more.

What is ITR 3?

ITR 3 means the Income Tax Return 3, which is a form that should be used by an individual and HUF who receives income from profits and gains from occupation or business. This will include a business or a profession, both tax audit and non-audit cases. The return includes income from house property, salary, pension, capital gains, and income from other sources.

Who can file ITR 3?

For the assessment year 2020- 2021, any individual taxpayer or a HUF is applicable to file the ITR3. Moreover, an individual taxpayer or a HUF who is earning income from a proprietary business or an individual who earns income from a profession during the financial year should file the ITR 3. In another scenario, Individual taxpayers’ or a HUF’s total income exceeds the amount that is not subject to income tax. Before enabling deductions under Chapter VI-A of the Income-tax Act, such income is determined. For each kind of taxpayer, the amount not subject to income tax is different. In case if the taxpayer’s total taxable income is not more than the basic exemption level but one or more of the following conditions are met, Form ITR 3 must be filed:

- If the taxpayer is in a director position of a company

- If the taxpayer has an investment which is unlisted equity shares during the financial year at any time.

- If the taxpayer is a partner of a firm and if he has income from the firm

- When the aggregates of the amount are more than one crore in one more current accounts that are held by the taxpayer

- When the taxpayer acquires a travel expense for a foreign trip either for himself or for any other person with the amount exceeding Rs 2 lakhs

- If the taxpayer incurs more than Rs 1 lakh for the expense of the consumption of electricity

- Individuals can additionally file income from wage or pension, income from other sources, and revenue from housing property while filing income from business or profession under ITR 3.

Who is not Required to File ITR 3 for 2021-2022?

When it comes to ITR 3 filings, there are certain factors to fulfill. Any individual taxpayer and HUF who are entitled to file ITR 1 Sahaj, ITR 2, or even ITR 4 Sugam will not be able to file ITR 3. They should file ITR1 Sahaj, ITR2, or ITR 4 Sugam as required based on the conditions given.

What is the Change in ITR 3 in 2021-22?

The major changes in ITR form 3 for 2021- 2022 are as follows:

- The recipient of a dividend will be required to pay tax from April 1, 2020. The Act has been revised to include relevant parts such as 10(34), 10(35), 115-O, and others. As a result, appropriate adjustments are made to the ITR form.

- If the dividend is not received, the taxpayers are exempt from paying the advance tax liability. As a result, the ITR form permits taxpayers to submit quarterly details of dividend income to compute interest under section 234C for failure to pay advance tax.

- If cash payments are less than 5% of total sales or turnover, the threshold limit for a tax audit is increased to Rs.10 crores from Rs.5 crores as amended by the Finance Bill 2021 in section 44AB. In the ITR form, the corresponding amendment is included.

- In the ITR form for AY 2021-22, the Schedule DI added for AY 2020-21 to claim deductions for investments or expenditures made in the extended period (1st April 2020 to 30th June 2020) has been eliminated.

- A new column is added to Schedule 112A and Schedule 115AD(1)(b)(iii) provisos to describe the kind of securities transferred to calculate capital gains tax under section 112A or section 115AD(1)(b)(iii) of the Income Tax Act. The schedules are also changed to allow the taxpayer to include information on the security’s sale price, fair market value, and cost of acquisition.

- When the taxpayer is offered the option of choosing a new tax system under section 115BAC, Part-A General Information is amended.

- The date of submitting Form No.10-IE and its acknowledgement number must be mentioned by the taxpayer who has income from a business or profession and is choosing an alternative tax regime.

How to file ITR 3?

People who want to file ITR 3 can do it online through the official website of Income Tax. Follow the steps given here to file your ITR 3 easily.

- Click on this link www.incometaxindiaefiling.gov.in to open the website and access the Income Tax e-Filing portal.

- Then log in to the e-filing portal. To do that you must enter the user ID (PAN) and password. You will be also asked to fill in the Captcha code and then click on the Login button. You must create an account on the income tax e-filing platform if you are a new user.

- After accessing your account, click on the e-file option

- Then select the Income-tax Return option from the drop-down menu

- Your PAN details will be automatically entered on the Income Tax Return Page

- The next step is to select the Assessment Year for which you want to file the ITR

- Select the ITR form number as ITR 3

- Select the Original option under the Filing Type. But if you are filing a revised return against an already filed original return, then you must select the option Revised Return

- Now select Prepare and Submit Online button under the Submission Mode

- Then click the Continue button

- You must now fill in the details of your income, deductions, exemptions, and your investments. Moreover, you should add the details of your tax payments through TDS/TCS, advance tax, and self-assessment tax.

- You must fill the schedule accurately, and you should save the draft so that you do not lose any data. To do that, just click on the Save Draft button. The saved data will be available for a month which is 30 days from the date you saved the file. But this draft will not be available once you file the ITR or if there is no change in the XML scheme of the ITR.

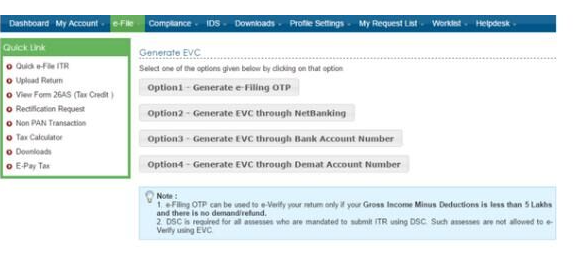

E-Verification Steps for ITR 3

- Select the verification choice under the Taxes Paid and Verification schedule section. You can e-verify and re-verify within 120 days or send a signed ITR- V through regular mail to the centralized processing centre, Income Tax Department, Bengaluru, within 120 days of filing the ITR. When you click on I would like to E-verify, then you can do it by entering the EVC/OTP ( EVC generated through bank ATM or generate EVC under My Account section, Aadhaar OTP, pre-validated Bank or Demat account) when asked.

- You must enter the EVC/OTP within 60 seconds; otherwise, the Income Tax Return will be auto-submitted. But you can verify the ITR later by logging in to your account.

- Then click on the Preview and Submit button to check and verify that the details you have entered are correct

- Click on the Submit button.

FAQs on ITR 3

- Will the IT department accept ITR3 filing by mail?

Ans: You can send the filled ITR 2 form by mail to the Income Tax Department at the following address. Post Bag No. 1, Electronic City Office, Bengaluru–560100.

- Do you need Aaadhaar for ITR3?

Ans: Aadhaar is a mandatory document required to file ITR3. You must give the Aadhaar details in the ITR 3 form while filing.

- What are the liabilities that should be declared in ITR 3?

Ans: If your total income from these sources exceeds Rs.50 lakhs, you must state value assets and liabilities on your ITR-3. All of your other immovable property, such as houses, jewellery, and gold bullion, must also be declared. In addition, you must declare any profit earned from other assets, such as shares and debentures as well.

- Is it mandatory to mention the nature of business in ITR 3?

Ans: It is necessary to include the details of your business like the nature of business, code of your business, trade name, and even a short description of your business. You must also include the details of the balance sheet filed as of March 31st of the financial year.

- What is unexplained income?

Ans: Unexplained income can include credit-earning or investment earning that should not be less than Rs. 10 lakhs to mention in the ITR.